News & Trends

The bottleneck of tomorrow

In the dust of mines and the heat of refineries, the pace at which the digital industry grows is decided. Lithium, nickel, cobalt, and graphite set the tempo – copper keeps the beat.

In a lithium brine field in Chile, brine evaporates in the heat of the Atacama until a concentrated salt mixture remains. In Indonesia, excavators move tons of nickel ore. And in Chinese industrial halls, raw materials are transformed into battery material that will later power an electric vehicle or stabilize a data center. This is where the digital industry takes shape.

Four so-called critical minerals form the heart of modern batteries: lithium, nickel, cobalt, and graphite. Without these four materials, there would be no large-scale electrification, no mobile robots, and no storage for renewable electricity.

“And yet these are niche metals,” says geologist and resource investor Fabian Erismann. The hidden king of electrification, he says, is another metal: copper. “Without copper, the world comes to a standstill.” Lithium, nickel, cobalt, and graphite sit inside the battery – copper conducts the electricity.

The four stages of power

Raw materials do not gain their strategic weight in the mine alone. Influence is determined along several stages of the value chain.

1. Extraction

Lithium is primarily mined in Australia and South America, cobalt mainly in the Democratic Republic of the Congo, and nickel in large quantities in Indonesia. Extraction is tied to specific locations – and politically sensitive ones. New mines are not developed on the timeline of election cycles. “Between discovery and the start of production, it often takes ten to fifteen years,” says Erismann. Neither the United States nor China fully controls access to the four raw materials. But China secured stakes early and built long-term supply relationships. The potential lies in the ground – what becomes of it is decided later.

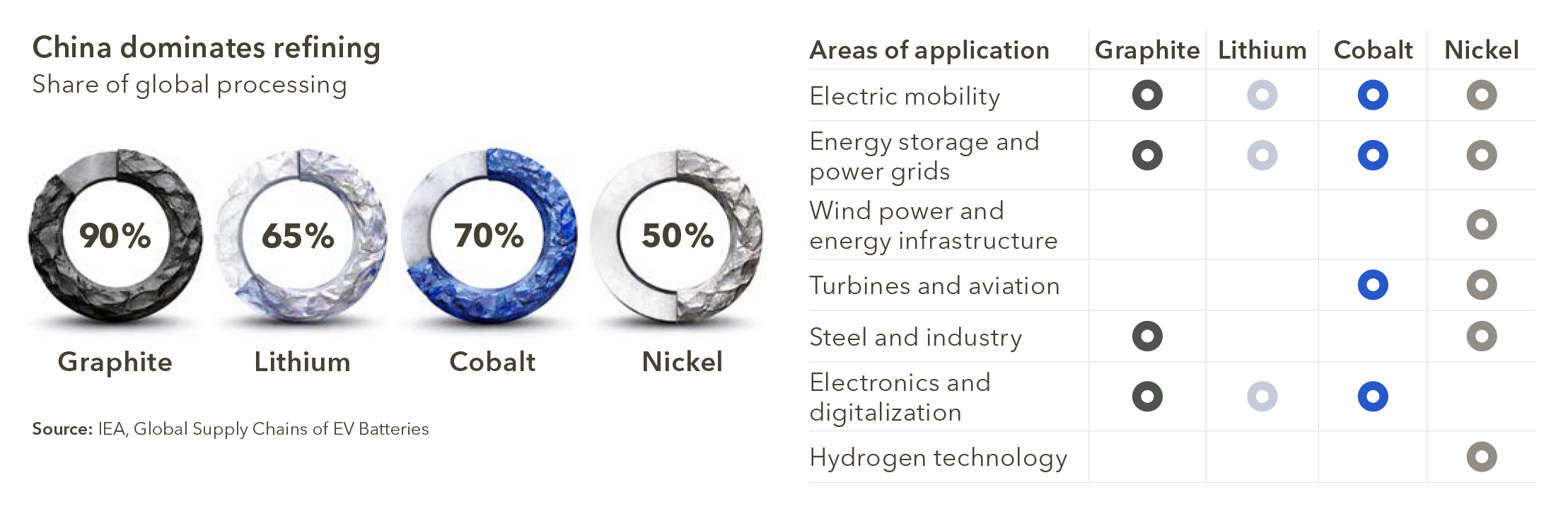

2. Processing

Ore or its concentrate alone does not make a battery. Only in refineries are the raw materials chemically processed so they can be used in battery cells. This is exactly where the bottleneck lies: “Around 95 percent of this part of the value chain is in Chinese hands,” says Erismann. Even material mined in Australia and South America is often further processed in Asia. Whoever controls this stage controls speed and prices.

3. Integration

After refining, the raw material is chemically upgraded, but it is still not a product. In manufacturing, battery cells are produced and installed in series production. “What matters is who is creating more value from the material,” says Erismann. Producing battery cells domestically secures know-how and strengthens control over supply chains. China recognized the importance of this step early. Erismann calls it “thinking through the value chain.” Individual steps do not have to be profitable on their own; what matters is the bigger picture. Europe and the United States often look at the chain in isolation.

4. Recycling

When batteries reach the end of their life, their metals can be recovered and reused. This reduces dependencies, but with a delay. Demand is growing faster than end-of-life material is becoming available. Recycling stabilizes the system, but it cannot replace new mines.

The time factor

The competition between the United States and China will be decided less by access to raw materials than by the speed at which projects are implemented. A new chip can be developed within a few years, but new mining projects require long lead times – from exploration to the first ton of material.

“The risk lies on the supply side,” says Erismann. “Today we rely on old mines that are losing quality.” New projects are technically complex and consume billions of dollars. Delays are more the rule than the exception – and even after production begins, output often falls short of expectations.

What does that mean? New technologies emerge quickly – but new mines do not. Without secure raw materials, progress is built on sand.

Value is created after extraction

Raw materials are only the beginning. What matters is where they are processed and turned into products. China expanded this value chain early. The United States is catching up, but processing remains largely in Chinese hands, and new mines take many years before they reach production.

In the end, electricity decides

Raw materials alone do not secure an industry. Fabian Erismann, Portfolio Manager at Earth Resource Investments, sheds light on the power of modern electricity grids.

Globalance View

The energy transition requires materials: batteries, solar installations, and wind turbines depend on metals and raw materials.

Efficiency is becoming key: recycling and better resource utilization reduce the need for new extraction.

Globalance invests in circular solutions: companies such as Umicore and Tomra are potential examples.

Discover the entire issue

Read more articles from our current issue: ‘The race of the operating systems’.

Be part of the solution and stay informed with the Futuremover.

Subscribe now and shape the future!

Magazin abonnieren EN

"*" indicates required fields